Samsara - Sensor Sensations

Highlighting Samsara's role in turning data into operational gold.

7/14/20245 min read

1. Company Overview and History

Samsara Inc. is a leading Internet of Things (IoT) company that provides a connected operations cloud platform to enable businesses to harness IoT data to develop actionable insights and improve their operations. Founded in 2015 by Sanjit Biswas and John Bicket, Samsara went public in 2021 and is headquartered in San Francisco, California.

The company's solutions serve customers across a variety of industries, including transportation, wholesale and retail trade, construction, field services, logistics, utilities and energy, government, healthcare, education, manufacturing, and food and beverage.

2. Business Model and Revenue Streams

Samsara's business model is based on providing a comprehensive IoT platform that combines hardware, software, and cloud-based analytics:

Hardware: Samsara designs and sells IoT devices such as vehicle telematics, equipment monitors, and site visibility cameras.

Software: The company's cloud-based software platform processes data from these devices and provides actionable insights.

Subscription Model: Samsara primarily generates revenue through subscription-based pricing for its connected operations cloud platform.

Revenue Breakdown (FY 2023):

By Product Type:

Subscription Revenue: 95%

License Revenue: 5%

By Customer Size (approximate):

Large Enterprises: 30%

Mid-Market: 50%

Small Business: 20%

By Industry (top industries):

Transportation and Logistics

Construction and Field Services

Utilities and Energy

Samsara does not provide a detailed geographic breakdown, but the majority of its revenue comes from North America.

3. Financial Performance and Growth Drivers

Samsara has demonstrated strong metrics:

Revenue CAGR (FY 2020-2023): 61.5%

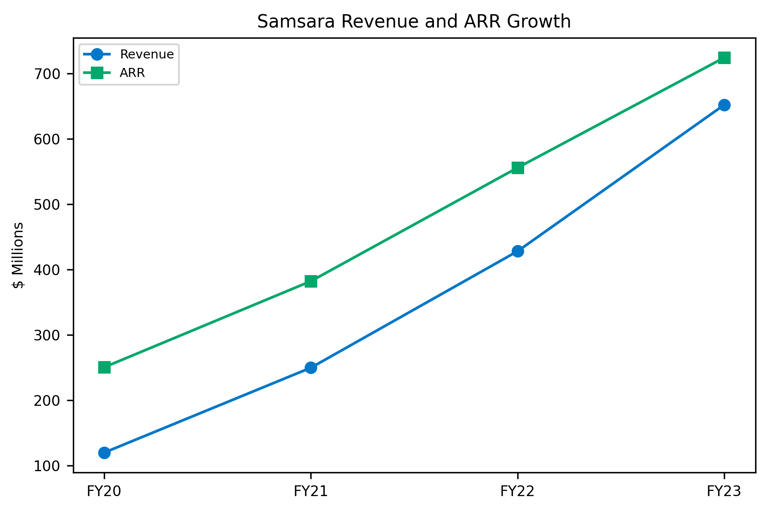

FY 2020 Revenue: $119.9 million

FY 2023 Revenue: $652.5 million

Gross Margin:

FY 2020: 71%

FY 2023: 73%

Annual Recurring Revenue (ARR) Growth:

FY 2023 ARR: $724.7 million (52% YoY growth)

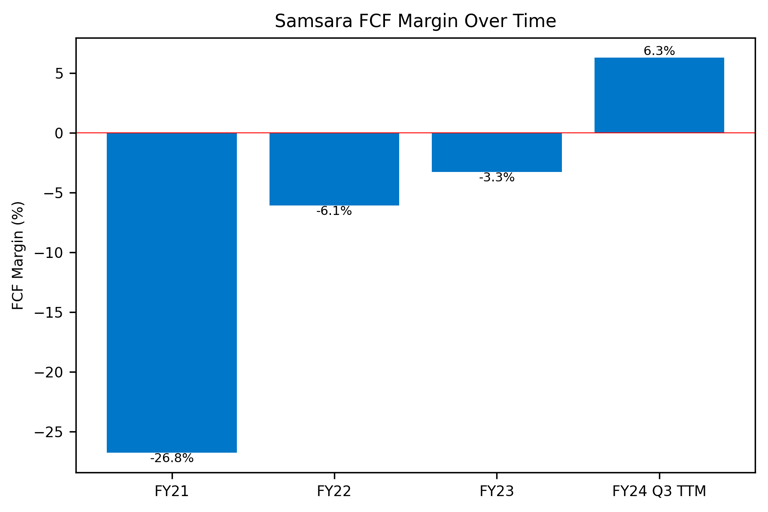

Free Cash Flow:

FY 2022: -$66.9 million

FY 2023: -$21.5 million (significant improvement)

Customer Metrics:

Total Customers:

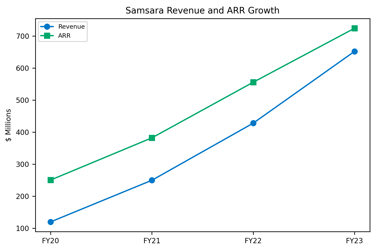

FY 2023: 27,000+ (up from 21,000+ in FY 2022)

Customers with ARR > $100,000:

FY 2023: 1,176 (up from 795 in FY 2022)

Retention and Expansion:

Net Retention Rate (NRR):

FY 2023: 129%

FY 2022: 124%

Sales Efficiency:

Magic Number (Q4 FY 2023): 1.16 (calculated as incremental ARR / S&M expense from previous quarter)

Profitability Metrics:

Non-GAAP Operating Margin:

FY 2023: -11% (improved from -25% in FY 2022)

Free Cash Flow Margin:

FY 2023: -3% (improved from -16% in FY 2022)

Key observations:

Strong Revenue Growth: Samsara's revenue has grown at an impressive CAGR of 75.8% from FY 2020 to FY 2023, demonstrating strong market demand for its products.

Improving Gross Margins: Gross margin has improved due to:

Economies of Scale: Increased purchasing power and manufacturing efficiencies.

Shift Towards Software: Higher proportion of software revenue compared to hardware.

Improved Free Cash Flow: Free Cash Flow is improving faster than revenue growth due to:

Operating Leverage: As revenue scales, fixed costs are spread over a larger base.

Improving Sales Efficiency: Reduced customer acquisition costs relative to customer lifetime value.

Subscription Model: Provides predictable, recurring revenue that translates well to cash flow.

Robust Customer Growth: The increase in total customers and those with ARR > $100,000 indicates successful customer acquisition across various segments.

High Net Retention Rate: The 129% NRR in FY 2023 suggests strong customer satisfaction and successful upselling/cross-selling efforts.

Improving Sales Efficiency: A magic number of 1.16 indicates good sales efficiency, with each dollar spent on sales and marketing generating more than a dollar in ARR.

Path to Profitability: While still operating at a loss, Samsara has significantly improved its operating and free cash flow margins, suggesting a clear path towards profitability.

These metrics collectively paint a picture of a rapidly growing company with improving efficiency and a strong ability to both acquire and retain customers. The high net retention rate is particularly noteworthy, as it indicates that existing customers are finding value in Samsara's products and increasing their usage over time.

Key growth drivers include:

Expansion Within Existing Customers: Samsara's net retention rate was 129% in FY 2023, indicating strong upselling and cross-selling.

New Customer Acquisition: The company has consistently grown its customer base, reaching 27,000+ customers in FY 2023.

Product Innovation: Continuous development of new features and capabilities to address evolving customer needs.

Market Expansion: Entering new geographic markets and industry verticals.

4. Competitive Landscape and Differentiation

The IoT and connected operations market is competitive and fragmented, with both established players and startups. Key competitors include:

Traditional telematics providers: Geotab, Verizon Connect

Industrial IoT companies: PTC, Siemens

Fleet management software providers: Fleetio, Samsara

General cloud platforms: Microsoft Azure IoT, AWS IoT

Samsara differentiates itself through:

Integrated Platform: Offers a comprehensive solution combining hardware, software, and analytics.

Ease of Use: Known for user-friendly interfaces and quick deployment.

AI and Machine Learning Capabilities: Provides advanced analytics and predictive insights.

Vertical-Specific Solutions: Tailored offerings for different industries.

Open Ecosystem: Integrates with a wide range of third-party applications.

Market Share: While exact figures are not publicly available, Samsara is considered a leader in the connected fleet and industrial IoT space, with an estimated market share of 10-15% in its core markets.

5. Future Growth Outlook

Samsara's future growth potential remains strong, driven by:

IoT Market Expansion: The global IoT market is expected to grow at a CAGR of 25.4% from 2022 to 2030 (Grand View Research).

Digital Transformation in Traditional Industries: Increasing adoption of IoT solutions in sectors like transportation, construction, and manufacturing.

Data Analytics and AI Advancements: Growing demand for predictive maintenance and operational optimization.

Geographic Expansion: Opportunities in international markets, particularly Europe and Asia.

New Product Development: Potential to address adjacent markets and use cases.

Projecting forward, we can estimate:

Revenue CAGR (FY 2024-2028): 30-35%

Gross Margin Improvement: Potential to reach 75-78% as software revenue increases

Path to Profitability: Expected to achieve GAAP profitability within the next 2-3 years

6. Management

Samsara's management team is led by its co-founders:

Sanjit Biswas (CEO and Co-founder): Previously co-founded Meraki (acquired by Cisco for $1.2 billion).

John Bicket (CTO and Co-founder): Also co-founded Meraki with Biswas.

Dominic Phillips (CFO): Joined in 2019, bringing experience from Concur and SAP.

Key Management Characteristics:

Founder-led: Both co-founders remain actively involved in the company's operations.

Technical Expertise: Strong background in networking and cloud technologies.

Track Record: Successful exit with previous venture (Meraki) demonstrates ability to build and scale technology companies.

7. Risks and Mitigations

Intense Competition:

Risk: Market fragmentation and potential for new entrants.

Mitigation: Continuous innovation, focus on customer success, and building a strong brand.

Hardware Dependency:

Risk: Reliance on hardware sales could impact margins and create supply chain vulnerabilities.

Mitigation: Shifting focus towards software and services, diversifying supplier base.

Economic Sensitivity:

Risk: Samsara's customers in transportation and construction are cyclical industries.

Mitigation: Diversification across industries and emphasis on cost-saving benefits of the platform.

Data Privacy and Security:

Risk: Handling sensitive customer data increases exposure to potential breaches.

Mitigation: Robust security measures, compliance with data protection regulations.

Profitability Concerns:

Risk: Current lack of GAAP profitability might concern investors.

Mitigation: Clear path to profitability, improving unit economics, and strong revenue growth.

In conclusion, Samsara's strong market position in the rapidly growing IoT sector, coupled with its high growth rates and improving financial metrics, make it an intriguing investment prospect. The company's integrated platform approach and focus on traditionally underserved industries provide a solid foundation for continued growth. However, investors should closely monitor Samsara's path to profitability and its ability to maintain its competitive edge in a dynamic market.