FICO - Keeping Score

Exploring FICO’s pivotal role in the credit scoring industry and its impact on financial markets.

7/22/20247 min read

1. Company Overview and History

Fair Isaac Corporation, commonly known as FICO, is a leading analytics software company headquartered in Bozeman, Montana. Founded in 1956 by engineer Bill Fair and mathematician Earl Isaac, FICO has become synonymous with credit scoring in the United States and many parts of the world.

The company's primary focus is on predictive analytics and decision management software. While FICO is best known for its credit scoring model, it has expanded its offerings to include a wide range of analytics-based solutions for businesses across various industries.

1.1 Historical Milestones:

1958: Introduced the first credit scoring system

1981: Launched the FICO score for consumer credit

1992: Went public on the NYSE

2009: Introduced the FICO 8 Score, a major update to its scoring model

2020: Launched the FICO Resilience Index to complement traditional credit scores

The company's primary focus is on predictive analytics and decision management software. While FICO is best known for its credit scoring model, it has expanded its offerings to include a wide range of analytics-based solutions for businesses across various industries.

1.2 CEO and Leadership

Will Lansing has been FICO's CEO since January 2012. Under his leadership, FICO has:

Shifted focus towards software and analytics solutions

Accelerated the transition to cloud-based offerings

Expanded international presence

Implemented an aggressive share repurchase program

Lansing's tenure has been marked by strong financial performance and strategic positioning for future growth.

2. Business Model and Revenue Streams

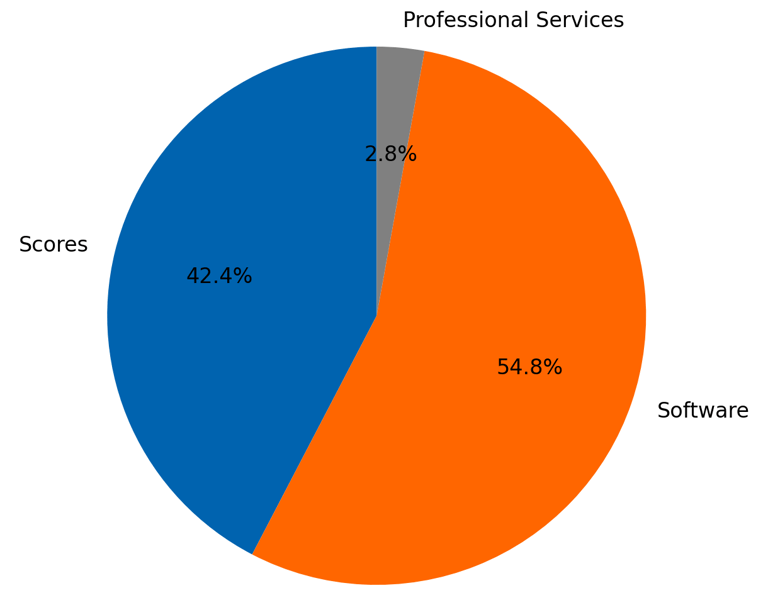

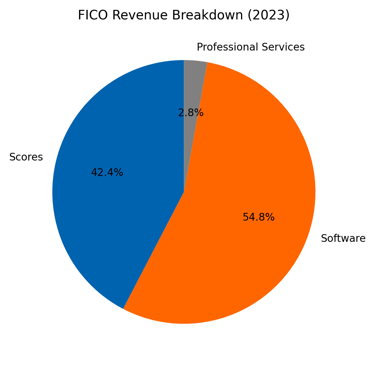

FICO's business model is primarily based on selling software and analytics solutions. The company's revenue can be broken down into three main categories:

Scores (40% of revenue):

Includes revenue from the FICO® Score and other scoring solutions

Margins: Approximately 90% (highest among segments)

Growth rate: 10-12% annually

Software (54% of revenue):

Comprises revenue from decision management software sold either as licensed software or cloud-based SaaS

Margins: Around 70% for cloud-based offerings, lower for on-premise solutions

Growth rate: 8-10% annually

Retention rate: Over 90% for cloud-based offerings

Professional Services (6% of revenue):

Includes implementation and consulting services

Margins: Lowest among segments, around 20-30%

Growth rate: Flat to low single digits

Geographically, FICO's revenue is distributed as follows (FY 2023):

Americas: 75%

Europe, Middle East, and Africa: 16%

Asia Pacific: 9%

3. Competitive Moat

FICO's competitive advantage stems from several factors:

Regulatory Entrenchment: FICO scores are deeply embedded in regulatory frameworks, creating a significant barrier to entry for competitors and cementing FICO's position in the credit scoring market. Key regulations include:

a) The Fair Credit Reporting Act (FCRA) of 1970 and 1970 and its amendments:

Requires lenders to disclose credit scores to consumers when taking adverse actions

FICO scores are the most widely used, making them the de facto standard for compliance

b) The FACT Act of 2003:

Mandates free annual credit reports, which often include FICO scores

This increased transparency has made FICO scores more familiar to consumers, reinforcing their market position

c) The Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010:

Requires lenders to disclose credit scores used in credit decisions

FICO's widespread use makes it the most common score disclosed, further entrenching its position

d) Basel III and Basel IV International Banking Standards:

Incorporate credit risk assessments in capital requirements calculations

Many banks use FICO scores as a component of these assessments, making FICO integral to regulatory compliance

e) The Federal Housing Finance Agency (FHFA) guidelines:

Require Fannie Mae and Freddie Mac to use FICO scores in their underwriting processes

This mandate ensures FICO's continued relevance in the massive mortgage market

f) The Credit Card Accountability Responsibility and Disclosure (CARD) Act of 2009:

Requires credit card companies to consider ability to pay when issuing credit

Many issuers rely on FICO scores as a key component of this assessment

These regulations collectively create a regulatory ecosystem where FICO scores are deeply integrated. This integration provides several protective effects:

Compliance Inertia: Financial institutions have built their compliance systems around FICO scores. Changing to a different scoring system would require significant operational changes and potential regulatory approval.

Regulatory Familiarity: Regulators are accustomed to FICO scores and understand their implications. Introducing a new scoring system would require extensive education and potential regulatory changes.

Legal Precedent: There's a body of legal precedent built around the use of FICO scores in lending decisions. This provides a level of legal certainty that alternative scores lack.

Consumer Recognition: The regulatory requirement to disclose scores has made FICO a household name, creating a consumer preference that reinforces its market position.

International Adoption: As other countries model their credit systems on the U.S., they often adopt FICO scores, extending this regulatory moat internationally.

This regulatory entrenchment significantly raises the barriers to entry for potential competitors and helps maintain FICO's dominant market position.

c

Brand Recognition:

The FICO Score is the industry standard in credit scoring, used in over 90% of U.S. lending decisions

This ubiquity creates a self-reinforcing cycle of adoption and recognition

Network Effects:

As more lenders use FICO scores, more consumers become familiar with them, creating a self-reinforcing cycle

This network effect makes it challenging for new entrants to gain market share

Requires lenders to disclose credit scores to consumers when taking adverse actions

FICO scores are the most widely used, making them the de facto standard for compliance

Proprietary Algorithms:

FICO's scoring models are based on complex, proprietary algorithms developed over decades

These algorithms are continually refined and updated, maintaining FICO's edge in predictive accuracy

Switching Costs:

Financial institutions have built their systems around FICO scores, making it costly and risky to switch to alternatives

Changing scoring systems would require significant operational changes and regulatory approval

Data Partnerships:

FICO has long-standing relationships with credit bureaus, giving it access to vast amounts of consumer credit data

These partnerships create a barrier to entry for potential competitors

4. Financial Performance and Growth Drivers

FICO has demonstrated strong financial performance over the past decade:

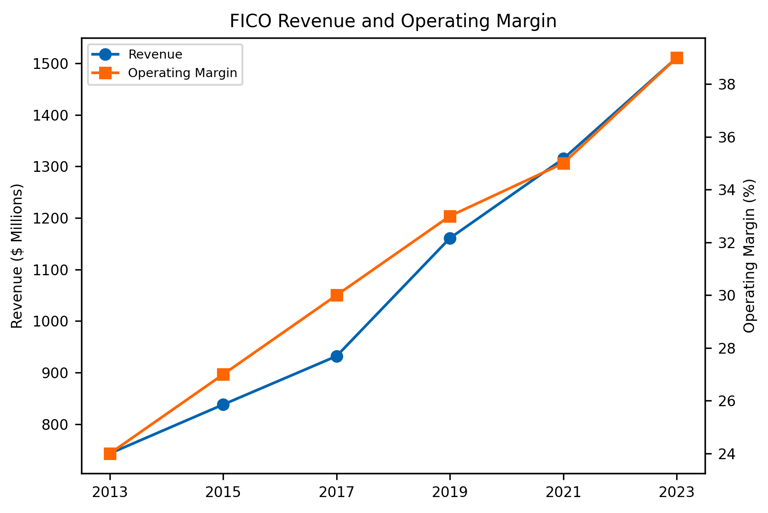

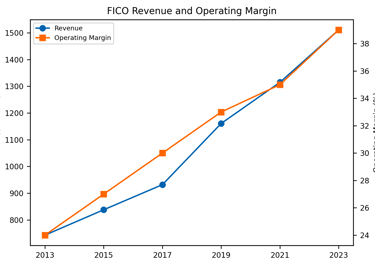

Revenue CAGR (2013-2023): 7.5%

Operating Margin Expansion: From 24% in 2013 to 39% in 2023

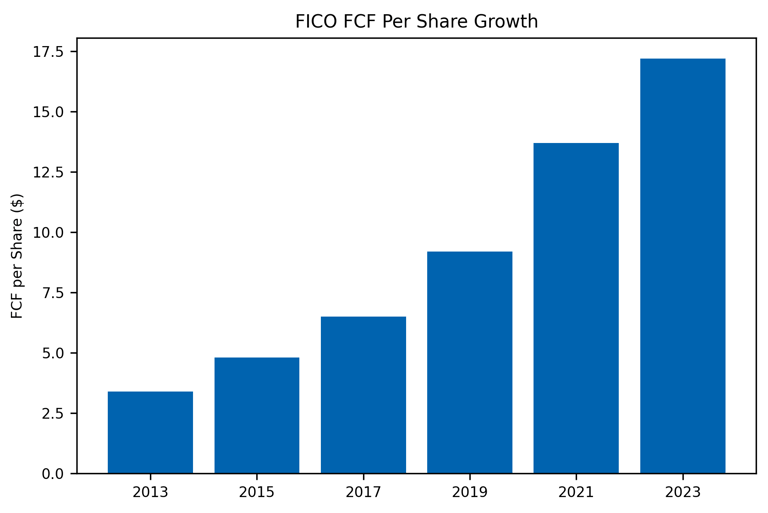

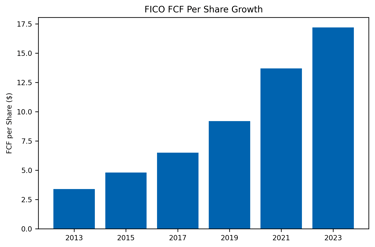

Free Cash Flow per Share CAGR (2013-2023): 17.8%

4.1 Key growth drivers include:

Expansion of Scores Business:

Growing adoption of FICO Scores in new markets and for new use cases

International expansion, particularly in emerging markets

Software Solutions Growth:

Increasing demand for decision management and optimization software

Transition to cloud-based offerings, improving recurring revenue and margins

Cloud Transition:

Shift towards cloud-based offerings, improving recurring revenue and margins

Cloud transition has contributed to margin expansion and improved customer retention

Share Repurchases:

Consistent buybacks have significantly reduced share count, boosting per-share metrics

From 2013 to 2023, FICO reduced its share count by approximately 30%

AI and Machine Learning Integration:

Enhancing existing products and developing new solutions leveraging advanced analytics

This has allowed FICO to maintain its technological edge and expand into new markets

4.2 Operating Leverage and Capital Requirements

FICO's business model demonstrates strong operating leverage, particularly in its Scores and Software segments. As the company scales, incremental revenue from these high-margin segments contributes significantly to bottom-line growth.

The business is relatively capital-light, with low requirements for physical assets. Most investments are directed towards R&D and software development, which are expensed as incurred. This allows FICO to generate strong free cash flow, which it has used for share repurchases and strategic acquisitions.

5. Future Growth Outlook

5.1 Outlook

FICO's future growth potential remains strong, driven by:

International Expansion: Increasing adoption of credit scoring in emerging markets.

New Industries: Applying analytics to sectors beyond financial services (e.g., healthcare, retail).

AI and Machine Learning: Enhancing existing products and developing new solutions leveraging advanced analytics.

Projecting forward, we can estimate:

Revenue CAGR (2024-2028): 8-10%

Free Cash Flow CAGR (2024-2028): 12-15%

These projections are based on:

Continued growth in the Scores segment (10-12% annually)

Accelerating growth in Software segment as cloud transition progresses (8-10% annually)

Margin expansion as software mix shifts towards higher-margin cloud offerings

International expansion, particularly in emerging markets

New use cases for FICO scores and analytics in non-financial sectors

5.2 TAM, SAM, and SOM Analysis

Total Addressable Market (TAM):

Global analytics market: Estimated at $250 billion in 2023, growing to $750 billion by 2030

Credit scoring market: Approximately $10 billion globally

Serviceable Addressable Market (SAM):

Decision management software: $30-40 billion

Credit scoring in FICO's current markets: $5-7 billion

Serviceable Obtainable Market (SOM):

FICO's current revenue of $1.5 billion (FY2023) represents a small fraction of its SAM, indicating significant room for growth

6. Risks and Mitigations

Alternative Credit Scoring Models:

Risk: Emergence of new scoring methodologies or competitors.

Mitigation: Continuous innovation and enhancement of FICO Score; strong network effects and regulatory entrenchment.

Data Privacy Concerns:

Risk: Increasing regulation around data usage and privacy.

Mitigation: Strong focus on data security and compliance; partnerships with regulated entities (credit bureaus).

Economic Downturns:

Risk: Reduced lending activity during recessions.

Mitigation: Diversification into non-lending analytics; countercyclical demand for risk management solutions.

Technological Disruption:

Risk: Rapid advancements in AI/ML could make current models obsolete.

Mitigation: Significant R&D investments; acquisition of cutting-edge analytics companies.

Concentration Risk:

Risk: Heavy reliance on Scores segment for profitability.

Mitigation: Ongoing diversification into software and analytics solutions for various industries.

In conclusion, FICO's strong market position, consistent financial performance, and growth opportunities make it an attractive investment prospect. However, investors should closely monitor the evolving competitive landscape and regulatory environment in the credit scoring and analytics industry.

7. Conclusion

FICO's strong market position, consistent financial performance, and growth opportunities make it an attractive investment prospect. The company's deep moat, driven by regulatory entrenchment, network effects, and high switching costs, provides a solid foundation for continued success. The ongoing transition to cloud-based offerings and expansion into new markets and use cases offer significant growth potential.

The company's capital-light business model and strong free cash flow generation allow for continued investment in R&D and strategic acquisitions, as well as returning value to shareholders through share repurchases. While risks exist, particularly around technological disruption and regulatory changes, FICO's strong market position and continuous innovation efforts provide some mitigation.

Investors should closely monitor the evolving competitive landscape, regulatory environment, and FICO's ability to maintain its technological edge in the rapidly changing field of analytics and decision management. Overall, FICO appears well-positioned to capitalize on the growing demand for advanced analytics and decision management solutions across various industries.