Cloudflare - Riding the Edge

Exploring how Cloudflare leverages edge computing to redefine internet infrastructure, providing enhanced security, speed, and scalability

8/15/202417 min read

1. Overview

1.1 What They Do

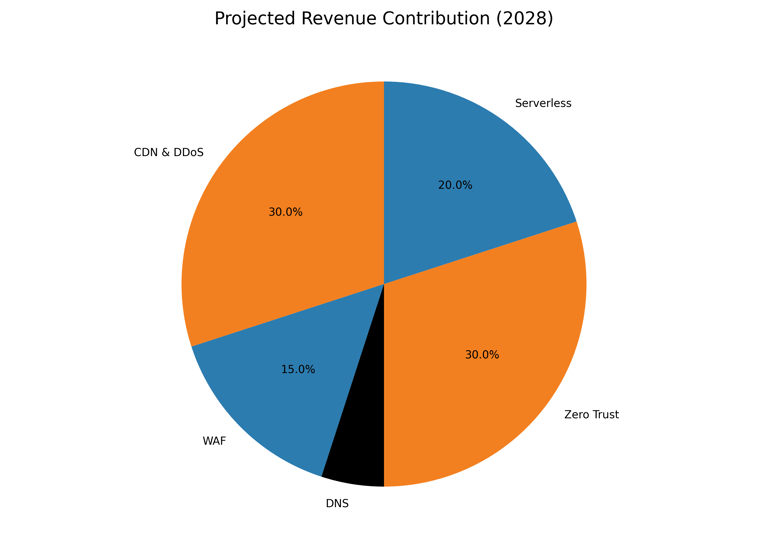

Cloudflare operates in the cloud computing and cybersecurity markets, providing a range of services that enhance the security, performance, and reliability of internet-connected systems. Their core offerings include:

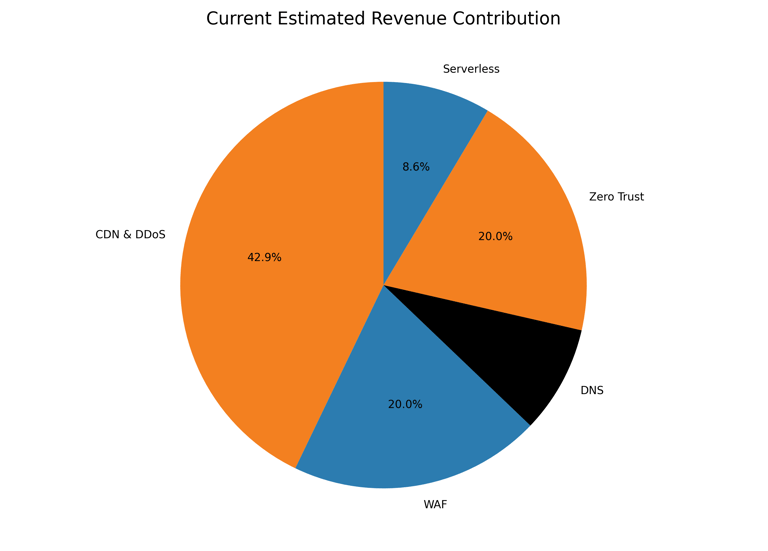

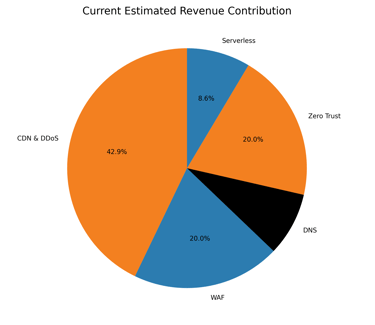

Content Delivery Network (CDN) and DDoS Mitigation

Estimated Revenue Contribution: 35-40%

Imagine you're running a popular online store. A CDN is like having multiple copies of your store spread out across the world. When a customer tries to access your website, they're directed to the nearest "store" (server), which means they get what they want faster. This makes your website load quickly for everyone, no matter where they are.

DDoS stands for Distributed Denial of Service. Imagine your store is suddenly flooded with thousands of fake customers who aren't buying anything but are blocking real customers from entering. DDoS mitigation is like having a team of security guards who can quickly spot these fake customers and keep them out, ensuring your real customers can always get in.

Core revenue driver and customer acquisition tool with continued growth potential as global internet traffic increases.

Web Application Firewall (WAF)

Estimated Revenue Contribution: 15-20%

Think of a WAF as a super-smart bouncer for your website. It checks every visitor (incoming web traffic) against a list of known troublemakers and suspicious behaviors. If someone tries to do something fishy, like inject malicious code or steal data, the WAF stops them before they can cause any harm.

Core revenue driver and customer acquisition tool with continued growth potential as global internet traffic increases.

DNS Services

Estimated Revenue Contribution: 5-10%

DNS is like the internet's phone book. When you type a website name (like www.example.com) into your browser, DNS services translate that into the actual numerical address (IP address) where the website is hosted. Cloudflare's DNS services make this process faster and more secure, like having an instant, always-updated phone book.

Essential infrastructure service that acts as a low-cost entry point, with potential for upselling and market share expansion.

Zero Trust Security

Estimated Revenue Contribution: 15-20%

Imagine a world where no one is automatically trusted, not even your own employees. Zero Trust Security is like having a strict bouncer who checks everyone's ID, no matter who they claim to be, every single time they try to access any part of your system. This approach assumes that threats can come from both outside and inside an organization, making it much harder for attackers to move around once they get in.

Fastest-growing segment addressing urgent enterprise security needs, representing a significant opportunity in the rapidly expanding cybersecurity market.

Serverless Computing (Cloudflare Workers)

Estimated Revenue Contribution: 5-10%

Traditional web hosting is like renting an entire apartment to run your business, even if you only need one room. Serverless computing, like Cloudflare Workers, is more like renting just the exact amount of space you need, exactly when you need it. You write your code, and Cloudflare takes care of all the infrastructure, scaling it up or down automatically based on demand. It's faster, often cheaper, and you only pay for what you use.

Strategic differentiator with high growth potential, particularly in AI/ML applications, fostering developer loyalty and enabling custom solutions.

1.2 Revenue Breakdown by Geography

Geographical revenue breakdown (Q2 2024):

United States: 51% ($204.5 million)

EMEA: 28% ($112.3 million)

APAC: 13% ($52.1 million)

Rest of World: 8% ($32.1 million)

2. History and Leadership

Cloudflare was founded in 2009 by Matthew Prince, Michelle Zatlyn, and Lee Holloway.

Matthew Prince and Lee Holloway initially created Project Honey Pot in 2004 to track online fraud and abuse. In 2009, they joined forces with Michelle Zatlyn to found Cloudflare, aiming to protect websites from attacks and improve performance. The idea was born out of the realization that they could use the data from Project Honey Pot to create a service that would protect any website. Cloudflare scaled rapidly by offering a free tier, which allowed them to gather vast amounts of data and improve their services while growing their customer base. Their focus on ease of use and quick setup also contributed to their rapid adoption.

Key milestones include:

2010: Public launch at TechCrunch Disrupt

2014: Raised $110 million in Series D funding

2019: IPO on September 13, priced at $15 per share

2021: Reached a market cap of over $50 billion

2023: Generated over $1 billion in annual revenue

2024 Q2: Crossed $1.6 billion in annualized revenue

Current leadership:

Matthew Prince: Co-founder and CEO

Michelle Zatlyn: Co-founder and COO

Thomas Seifert: CFO

2.1 CEO Profile: Matthew Prince

Matthew Prince, co-founder and CEO of Cloudflare, has been instrumental in the company's growth and success:

Visionary leadership: Prince has consistently anticipated market trends, leading Cloudflare into new areas like edge computing and Zero Trust security.

Technical expertise: With a background in computer science, Prince has a deep understanding of the technology underlying Cloudflare's products.

Industry influence: Prince is a respected figure in the cybersecurity and internet infrastructure space, often speaking at industry events and engaging with policymakers.

Long-term focus: Under Prince's leadership, Cloudflare has prioritized long-term growth and innovation over short-term profitability.

Customer-centric approach: Prince regularly engages with customers and emphasizes the importance of customer trust and satisfaction.

Prince's continued leadership is a key factor in Cloudflare's future prospects, given his track record of strategic decision-making and ability to attract top talent to the company

3. Market Position and Moat

3.1 Market Share

CDN market: Estimated 15-20% share

DDoS mitigation: Among top 3 providers globally

DNS services: Over 1 million domains using Cloudflare DNS

3.2 Moat Drivers

Network effects: With over 4 million customers, Cloudflare's threat intelligence improves with each new user.

Economies of scale: Global network spans over 330 cities in 120+ countries.

Technological innovation: Over 1,000 developers and 500+ patents.

Customer stickiness: Dollar-based Net Retention Rate of 112% in Q2 2024.

3.3 Pricing Power

Evidence of pricing power includes:

Increasing number of $100k+ customers (3,046 in Q2 2024, up 30% YoY)

Rising average revenue per customer ($17,820 in 2023, up from $16,360 in 2022)

Ability to introduce new, premium-priced services (e.g., Magic WAN, Zero Trust)

3.4 Main Competitors

Akamai Technologies

Fastly

Amazon CloudFront (AWS)

Google Cloud CDN

Zscaler (in Zero Trust)

Cisco Umbrella

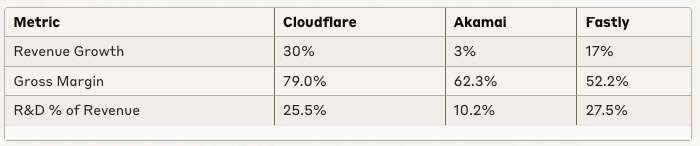

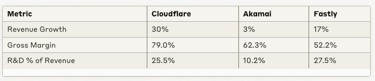

3.5 Competitive Comparison (2023 data)

3.6 Cloudflare's Competitive Advantages

Cloudflare outperforms many competitors in terms of growth and margins for several reasons:

Newer, more efficient architecture: Cloudflare's software-defined network is more cost-effective than legacy hardware-based approaches.

Broader product portfolio: Cloudflare offers a more comprehensive suite of services, allowing for better cross-selling and higher margins.

Focus on innovation: Higher R&D spend (25.5% of revenue) leads to more advanced products that command premium pricing.

Economies of scale: Cloudflare's rapid growth allows it to negotiate better rates with providers and spread fixed costs over a larger revenue base.

3.7 Defense Against AWS and Google Cloud

Despite competition from tech giants like AWS and Google Cloud, Cloudflare maintains its position due to:

Neutrality: Cloudflare is not tied to any specific cloud provider, appealing to customers seeking multi-cloud or cloud-agnostic solutions.

Specialization: Cloudflare focuses solely on edge computing and security, allowing for deeper expertise and faster innovation.

Developer focus: Cloudflare's products like Workers are more developer-friendly, fostering a loyal community.

Integrated platform: Offers a comprehensive suite of services on a single platform, reducing complexity for customers.

Disruptive pricing: Often introduces products at lower price points (e.g., R2 object storage with no egress fees).

Global network: Presence in 330+ cities globally, often providing better performance than larger competitors in certain regions.

4. Financial Profile and Growth

4.1 Key Performance Indicators

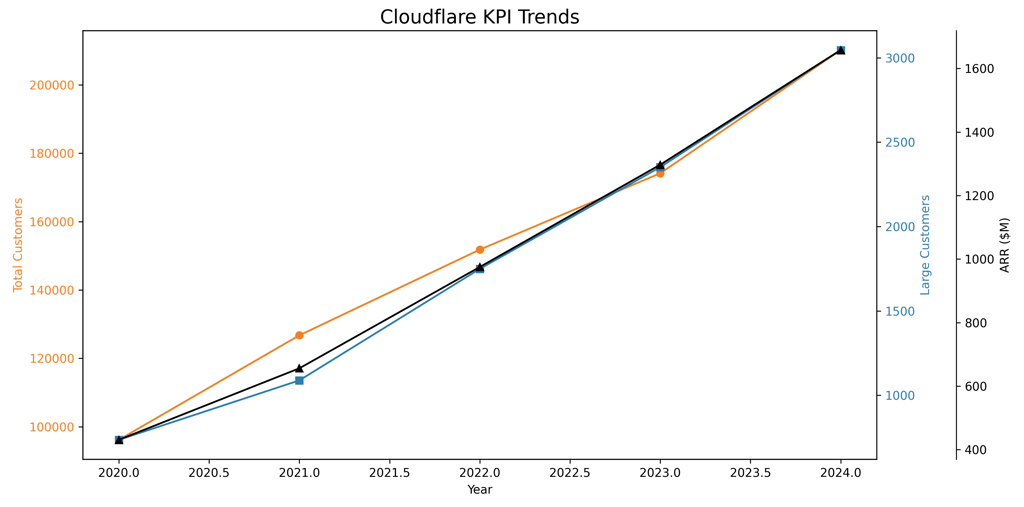

Paying Customers:

Q2 2024: 210,166 (21% YoY growth)

Q2 2023: 174,129

Q2 2022: 151,803

Q2 2021: 126,735

Q2 2020: 96,178

Large Customers (>$100k annually):

Q2 2024: 3,046 (30% YoY growth)

Q2 2023: 2,352

Q2 2022: 1,749

Q2 2021: 1,088

Q2 2020: 736

Dollar-based Net Retention Rate:

Q2 2024: 112%

Q2 2023: 115%

Q2 2022: 126%

Q2 2021: 124%

Q2 2020: 115%

Annual Recurring Revenue (ARR):

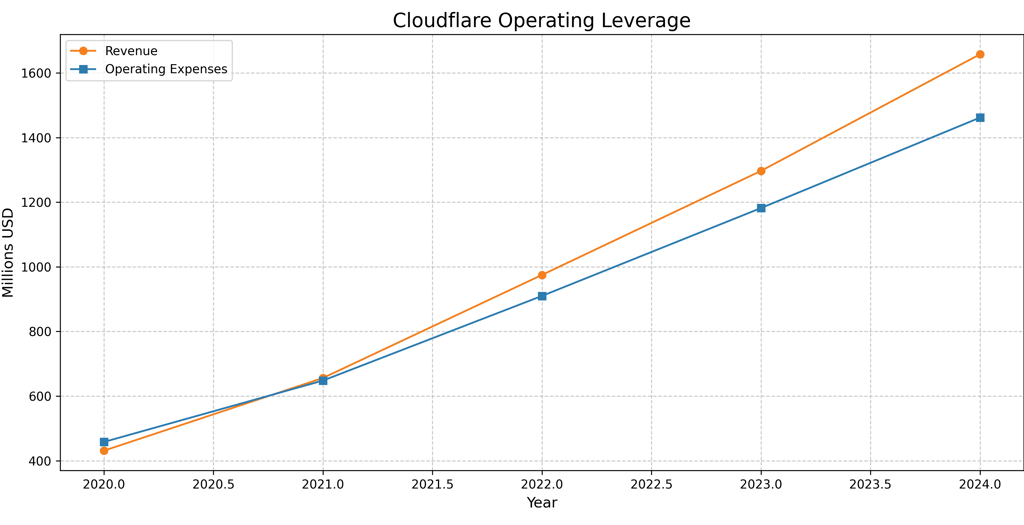

2024 (projected): $1,658 million

2023: $1,297 million

2022: $975 million

2021: $656 million

2020: $431 million

Rule of 40:

Q2 2024: 44.2% (30% revenue growth + 14.2% operating margin)

2023: 39.2% (30% revenue growth + 9.2% operating margin)

2022: 52.7% (49% revenue growth + 3.7% operating margin)

2021: 52.7% (52% revenue growth + 0.7% operating margin)

2020: 51.6% (50% revenue growth + 1.6% operating margin)

4.2 Financial Metrics

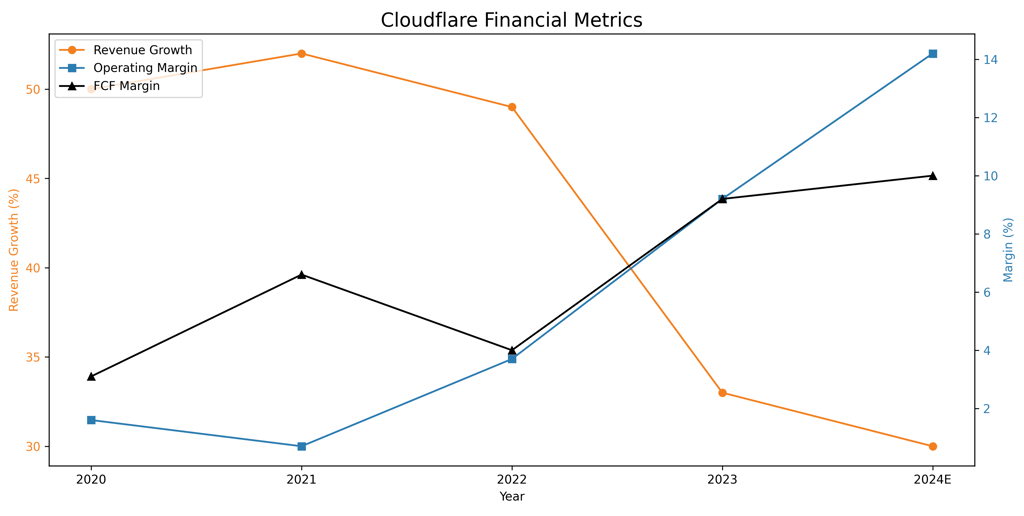

Revenue Growth:

Q2 2024: 30% YoY

2023: 33% YoY

2022: 49% YoY

2021: 52% YoY

2020: 50% YoY

Gross Margin (Non-GAAP):

Q2 2024: 79.0%

2023: 79.0%

2022: 78.5%

2021: 78.2%

2020: 77.6%

Operating Margin (Non-GAAP):

Q2 2024: 14.2%

2023: 9.2%

2022: 3.7%

2021: 0.7%

2020: 1.6%

Free Cash Flow (FCF) Margin:

Q2 2024: 10.0%

2023: 9.2%

2022: 4.0%

2021: 6.6%

2020: 3.1%

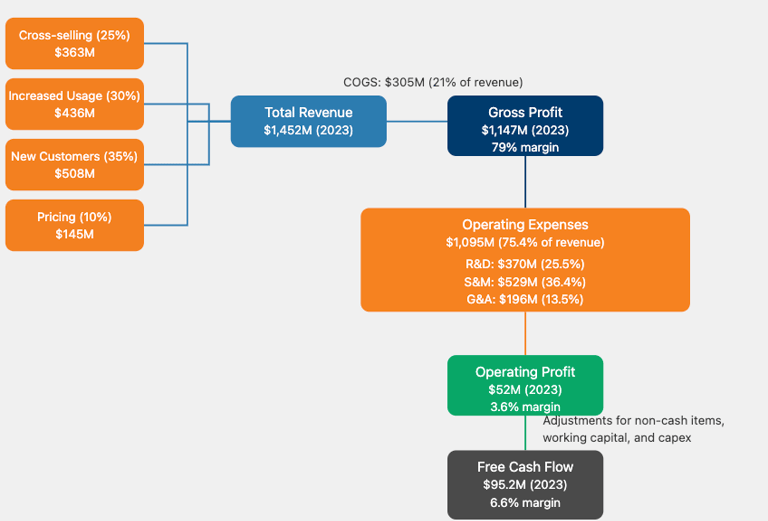

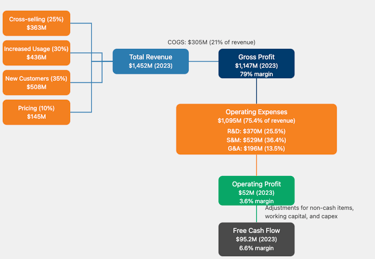

COGS and OpEx Breakdown:

Cost of Goods Sold (COGS):

Bandwidth and colocation fees

Depreciation of network equipment

Personnel costs for network operations team

Third-party licensing fees

Operating Expenses (OpEx):

Sales and Marketing:

Sales team compensation

Marketing campaigns and events

Customer support

Research and Development:

Engineering salaries

Cloud computing costs for development

Software licenses and tools

General and Administrative:

Executive compensation

Legal and accounting fees

Office expenses and rent

Insurance

Cloudflare's ability to improve margins while maintaining high growth relies on efficiently managing these costs while scaling revenue. The company's software-defined networking approach and focus on automation help control COGS, while improvements in sales efficiency and product-led growth strategies aim to optimize OpEx.

4.3 Drivers of KPI and Financial Performance

Product Expansion:

Continuous introduction of new services (e.g., R2 storage, D1 database, AI/ML offerings)

Broadening of Zero Trust and edge computing capabilities

Market Expansion:

Increasing presence in enterprise segment

Growing international market share (49% of revenue from outside the U.S. in Q2 2024)

Upselling and Cross-selling:

Success in moving customers to higher-tier plans

Adoption of multiple products by existing customers

Industry Trends:

Growing importance of cybersecurity and web performance

Shift towards edge computing and serverless architectures

Increasing demand for AI/ML capabilities at the edge

Operational Efficiency:

Economies of scale in network infrastructure

Improving sales efficiency and go-to-market strategies

Optimization of R&D investments

4.4 Pricing Model and Cash Flow Cycle

Pricing Model

Cloudflare offers a tiered pricing model that caters to a wide range of customers, from individual developers to large enterprises:

Cloudflare offers a tiered pricing model:

Free Tier

Pro Plan (e.g., $20/month)

Business Plan (e.g., $200/month)

Enterprise Plan (custom pricing)

Usage-Based Pricing for certain products

Free Tier:

Basic services at no cost

Serves as a customer acquisition tool and allows users to test basic functionalities

Pro Plan:

Fixed monthly fee (e.g., $20/month)

Targeted at small businesses and professional websites

Business Plan:

Higher fixed monthly fee (e.g., $200/month)

Includes more advanced features and support

Enterprise Plan:

Custom pricing based on specific needs and usage

Typically involves annual or multi-year contracts

Usage-Based Pricing:

Applies to certain products (e.g., Workers, R2 storage)

Customers pay based on their actual usage of resources

How Cloudflare Charges Customers

Subscription-Based Billing:

Pro and Business plans are typically billed monthly or annually

Enterprise plans are often billed annually or according to custom contract terms

Usage-Based Billing:

For products like Workers or R2, customers are billed based on their actual usage

Bills are typically generated monthly for usage-based services

Pool of Funds Model:

Increasingly common for large enterprise customers

Customers commit to a certain spend over a contract period (often multi-year)

Allows flexibility in using various Cloudflare services up to the committed amount

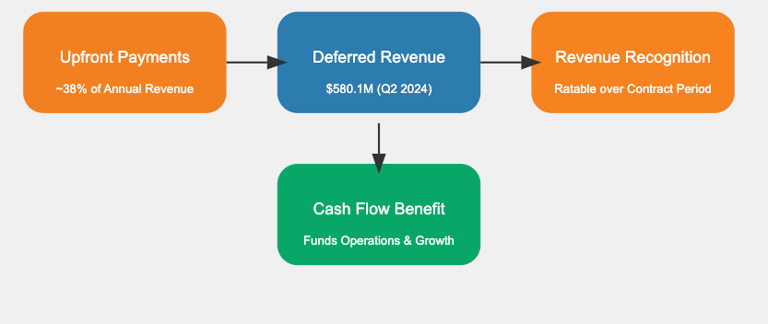

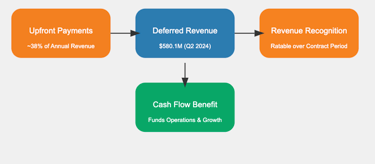

Upfront Payments:

Some customers, especially those on annual plans, may pay upfront for the entire year

This provides Cloudflare with cash flow advantages

Upfront Revenue and Impact on Cash Flow Cycle

Cloudflare receives a significant portion of its revenue upfront, which has a substantial impact on its cash flow cycle. Let's break this down:

Proportion of Upfront Revenue: While Cloudflare doesn't disclose the exact percentage of revenue received upfront, we can estimate based on their financial statements and industry norms:

Deferred Revenue: As of Q2 2024, Cloudflare reported:

Current deferred revenue: $568.2 million

Non-current deferred revenue: $11.9 million

Total deferred revenue: $580.1 million

Compared to trailing twelve-month revenue of $1,526 million, this suggests that approximately 38% of annual revenue is collected in advance.

Sources of Upfront Revenue:

Annual subscriptions for Pro and Business plans

Enterprise contracts with annual or multi-year prepayments

"Pool of funds" deals where large customers commit to significant spend upfront

Impact on Cash Flow Cycle: a) Positive Cash Flow Impact:

Accelerated cash collection: Cloudflare receives cash before delivering services

Q2 2024 operating cash flow: $120.4 million (30% of quarterly revenue)

This strong cash generation is partly due to the high proportion of upfront payments

b) Deferred Revenue Recognition:

Revenue is recognized ratably over the contract period

Creates a lag between cash receipt and revenue recognition

c) Working Capital Advantage:

Negative working capital model: Cloudflare can use customer prepayments to fund operations and growth

Reduces reliance on external financing for day-to-day operations

d) Predictable Cash Flows:

Upfront payments provide visibility into future cash flows

Helps in planning for investments and managing expenses

Financial Metrics Influenced by Upfront Payments: a) Remaining Performance Obligations (RPO):

Total RPO as of Q2 2024: $1,421 million

Represents future revenue under contract, often with cash already collected

69% expected to be recognized as revenue within the next 12 months

b) Billings:

While Cloudflare doesn't report billings directly, it can be estimated: Billings ≈ Revenue + Change in Deferred Revenue

High billings relative to revenue indicate strong upfront collections

Year-over-Year Trends:

Q2 2024 deferred revenue: $580.1 million, up 20% YoY

This growth in deferred revenue, while slower than revenue growth (30% YoY), still indicates strong upfront payments

Cash Flow Cycle Visualization:

x

Impact on Financial Strategy:

Allows for aggressive investment in growth without diluting shareholders through equity issuances

Provides a buffer against short-term market fluctuations or economic downturns

Enables strategic long-term planning and investment in innovation

Potential Risks:

Deferred revenue could decline if customers shift to shorter contract terms or usage-based pricing

Economic downturns could lead to fewer upfront commitments, impacting cash flow

Accounting scrutiny: Ensuring proper revenue recognition practices for complex contracts

In conclusion, Cloudflare's high proportion of upfront revenue significantly enhances its cash flow cycle, providing financial flexibility and supporting its growth strategy. This model allows Cloudflare to fund its operations and investments efficiently, contributing to its strong market position and ability to innovate rapidly. However, it's important for investors to monitor the trends in deferred revenue and contract terms, as changes could signal shifts in Cloudflare's cash flow dynamics.

4.5 Capital Light Business Model

Cloudflare's business is considered capital light due to:

Software-centric approach: Unlike traditional CDN providers, Cloudflare doesn't own massive amounts of physical infrastructure.

Efficient use of commodity hardware: Cloudflare's software-defined network runs on standard servers, reducing hardware costs.

Decreasing capex intensity: 6% of revenue in Q2 2024, expected to reach 10-12% for full year 2024.

Leveraging of third-party data centers: Cloudflare collocates its equipment in existing data centers rather than building its own.

4.6 Operating Leverage

Evidence of operating leverage:

Factors contributing to operating leverage:

Scalable infrastructure: The cost of serving additional customers on existing infrastructure is low.

Improving gross margins: As Cloudflare grows, it can negotiate better rates with bandwidth providers.

Efficient sales model: The self-serve model allows for customer acquisition with minimal incremental cost.

Increasing enterprise penetration: Larger deals with enterprises drive revenue growth faster than cost growth.

5. Growth Drivers and Opportunities

5.2 Traditional Growth Drivers

Breakdown of factors contributing to the 30% growth rate in Q2 2024:

Up/cross-selling to existing customers: ~25% (7.5 percentage points)

Introduction of new products (e.g., R2, D1)

Expansion of Zero Trust offerings

Increased usage by existing customers: ~30% (9 percentage points)

Organic growth of customer businesses

Increased reliance on digital infrastructure

New customer acquisition: ~35% (10.5 percentage points)

Expansion into new markets

Growing awareness of cybersecurity needs

Pricing adjustments: ~10% (3 percentage points)

Strategic price increases for certain services

Introduction of premium tiers

5.2 LLM and AI Opportunities

Cloudflare is well-positioned to benefit from the growth of Large Language Models (LLMs) and AI:

AI Inference at the Edge:

Cloudflare's global network allows for low-latency AI inference close to end-users

As of Q2 2024, Cloudflare had inference-tuned GPUs in 167 cities worldwide

AI Developer Platform:

Workers AI platform enables developers to build AI-powered applications

Cloudflare reported a 67% quarter-over-quarter increase in developer accounts using AI functions

AI-Driven Security:

Leveraging AI to enhance threat detection and mitigation capabilities

Potential for more sophisticated bot detection and API security

AI Infrastructure Services:

Providing the underlying infrastructure for AI model training and deployment

R2 object storage can be used for storing large datasets required for AI training

AI Compliance and Regulation:

Cloudflare's global presence and focus on compliance position it well to address emerging AI regulations

Ability to offer region-specific AI services to meet data localization requirements

AI-Enhanced Product Offerings:

Integrating AI capabilities into existing products to provide more intelligent CDN, security, and performance optimizations

These AI-related opportunities are expected to contribute increasingly to Cloudflare's growth in the coming years, potentially accelerating adoption of its platform and opening new revenue streams.

5.3 TAM, SAM, and SOM Analysis

Total Addressable Market (TAM)

Cloudflare estimates its Total Addressable Market (TAM) to reach approximately $176 billion in 2024. This figure is derived from various market segments that Cloudflare's products address. Let's break down the TAM calculation based on industry reports and Cloudflare's own estimates:

Application Services: $72 billion

Web Application Firewalls: $2.8 billion (Source: MarketsandMarkets)

DDoS Protection: $4.5 billion (Source: MarketsandMarkets)

CDN: $19.2 billion (Source: MarketsandMarkets)

DNS Services: $0.5 billion (Source: Global Market Insights)

Bot Management: $2.5 billion (Source: MarketsandMarkets)

API Security: $42.5 billion (Source: KBV Research)

Zero Trust Services: $38 billion

Zero Trust Network Access: $15.6 billion (Source: MarketsandMarkets)

Secure Web Gateway: $6.5 billion (Source: MarketsandMarkets)

Cloud Access Security Broker: $7.5 billion (Source: MarketsandMarkets)

Email Security: $6.8 billion (Source: MarketsandMarkets)

Data Loss Prevention: $1.6 billion (Source: Grand View Research)

Network Services: $66 billion

SD-WAN: $8.4 billion (Source: IDC)

Network-as-a-Service: $15.8 billion (Source: Allied Market Research)

Network Analytics: $3.1 billion (Source: MarketsandMarkets)

Network Security: $38.7 billion (Source: MarketsandMarkets)

Total: $72 billion + $38 billion + $66 billion = $176 billion

It's important to note that these figures are estimates and may overlap in some areas. Cloudflare's approach to calculating TAM is based on its current product offerings and may evolve as the company expands into new markets or develops new services.

Serviceable Addressable Market (SAM)

To calculate the Serviceable Addressable Market (SAM), we need to consider Cloudflare's current capabilities, target customer segments, and geographical reach. Based on the company's focus on internet-centric businesses and its global presence, we can estimate the SAM to be approximately 60% of the TAM.

SAM Calculation: $176 billion (TAM) * 60% = $105.6 billion

Rationale for 60% estimate:

Geographical reach: Cloudflare operates in over 100 countries but may not have full market access in all regions.

Customer focus: While Cloudflare serves businesses of all sizes, it may not target certain segments (e.g., very small businesses or specific industries) as effectively as others.

Product maturity: Some of Cloudflare's offerings are more mature and competitive than others, affecting their ability to address the full market.

Serviceable Obtainable Market (SOM)

Given Cloudflare's current market position and growth trajectory, we can estimate their SOM for 2024 to be around $1.7 billion (based on their 2024 revenue guidance).

Market Penetration and Growth Potential:

Current market penetration (SOM/SAM): ~1.6%

5-year projected market penetration (2028 revenue estimate / 2024 SAM): ~3.8%

This analysis suggests significant room for growth within Cloudflare's addressable market. The company's projected revenue growth aligns with increasing market penetration, supported by its expanding product portfolio and market presence.

7.Outlook

7.1 Revenue Projections

Based on Cloudflare's Q2 2024 earnings, guidance, and adjusted future estimates:

2024: $1,658 million (28% YoY, based on guidance midpoint)

2025: $2,123 million (28% YoY, estimated)

2026: $2,674 million (26% YoY, estimated)

2027: $3,316 million (24% YoY, estimated)

2028: $4,047 million (22% YoY, estimated)

Breakdown of factors contributing to projected growth rates:

New customer acquisition:

2024: 12% (of total growth)

2025-2028: Gradually decreasing from 11% to 8% as the customer base matures

Expansion within existing customers:

2024: 10% (of total growth)

2025-2028: Increasing from 11% to 13% as cross-selling and upselling efforts mature

Increased usage by existing customers:

2024: 5% (of total growth)

2025-2028: Stable at 5-6% as customers continue to rely more on Cloudflare's services

Introduction of new products and services:

2024: 1% (of total growth)

2025-2028: Increasing from 2% to 4% as new offerings gain traction

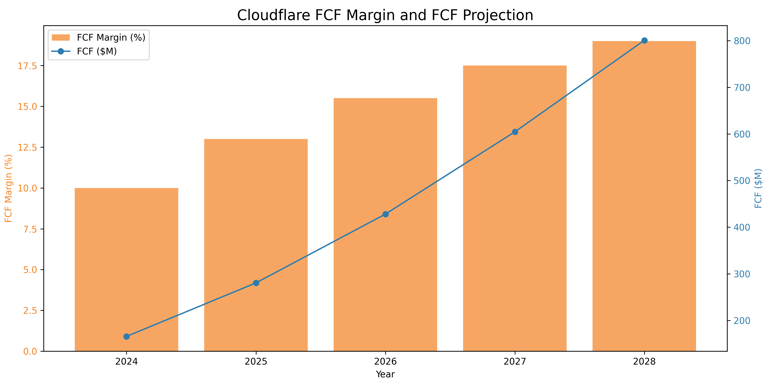

7.2 FCF Margin Projection

2024: 10.0% (based on guidance)

2025: 13.0% (+3.0%)

2026: 15.5% (+2.5%)

2027: 17.5% (+2.0%)

2028: 19.0% (+1.5%)

Clouflare is targeting a long-term FCF margin of around 25%. Hence, reaching 19% by 2028 appears realistic.

Explanation of margin increases:

2025: +3.0%

Significant operating leverage as revenue scales

Improved efficiency in sales and marketing spend

Continued optimization of network infrastructure

2026: +2.5%

Further operating leverage, though at a slightly slower pace

Increased contribution from higher-margin products (e.g., Zero Trust, Workers)

Economies of scale in R&D and G&A expenses

2027: +2.0%

Continued but moderating operating leverage

Maturation of key markets leading to more efficient customer acquisition

Ongoing improvements in working capital management

2028: +1.5%

Slower improvement as the company reaches larger scale

Potential for increased competition in key markets

Continued investment in innovation to maintain market position

Projected Free Cash Flow: (Assuming 30% YoY revenue growth)

2024: $166 million

2025: $281 million

2026: $428 million

2027: $604 million

2028: $801 million

Key drivers of FCF margin expansion:

Gross margin improvement: Expected to stabilize around 79-80% due to efficient infrastructure and economies of scale.

Sales and marketing efficiency: As the brand strengthens and the partner ecosystem matures, customer acquisition costs are expected to decrease relative to revenue.

R&D leverage: While continuing to invest heavily in innovation, R&D spend as a percentage of revenue is expected to decrease slightly as the product portfolio matures.

G&A leverage: Administrative costs are expected to grow slower than revenue as the company scales.

Working capital management: Improved efficiency in managing accounts receivable and payable is expected to contribute to FCF growth.

Capital expenditure optimization: While absolute capex may increase, it's expected to decrease as a percentage of revenue, contributing to FCF margin expansion.

This FCF margin expansion model assumes that Cloudflare will successfully execute its growth strategy while maintaining disciplined cost management. However, it's important to note that actual results may vary based on market conditions, competitive dynamics, and the company's strategic decisions.

Potential uses of cash flow:

Reinvestment in R&D to maintain technological edge

Expansion of global network infrastructure

Strategic acquisitions to enhance product offerings or enter new markets

Share repurchases to return value to shareholders

Building cash reserves for financial flexibility

Market Penetration and Growth Potential

Given Cloudflare's projected revenue growth, we can estimate future market penetration:

2024 (current): 1.57% of SAM

2028 projection: $4.047 billion / $105.6 billion ≈ 3.83% of 2024 SAM

This analysis suggests significant room for growth within Cloudflare's addressable market. The company's projected revenue growth aligns with increasing market penetration, supported by its expanding product portfolio and market presence.

Key factors that could influence Cloudflare's ability to capture more of its SAM include:

Continued product innovation, especially in high-growth areas like Zero Trust and AI services

Expansion of enterprise customer base

Increased penetration in international markets

Success in cross-selling and upselling to existing customers

Competitive dynamics and Cloudflare's ability to maintain technological advantages

It's important to note that as Cloudflare grows and introduces new products, its TAM and SAM may also expand, potentially providing even more room for growth beyond these current estimates.

Valuation:

Cloudflare trades at a premium valuation compared to most of its peers. This premium may be justified by:

Strong revenue growth (30% YoY) compared to traditional CDN providers like Akamai (3% YoY).

Higher gross margins (79%) compared to competitors like Fastly (52.2%).

Broader product portfolio and potential for cross-selling and upselling.

Significant TAM and growth runway in emerging areas like Zero Trust and edge computing.

AI and LLM opportunities that could accelerate growth in the coming years.

However, investors should consider:

The valuation leaves little room for execution errors.

Potential competition from well-resourced cloud giants like AWS and Google Cloud.

The need for continued innovation to maintain its technological edge.

8. Risks

Intense Competition:

Large tech giants (AWS, Google) have significant resources to compete.

Potential for price wars in commoditized services like CDN.

Risk of falling behind in rapidly evolving technology landscape.

Service Disruptions:

Any major outage could harm reputation and lead to customer churn.

Example: June 2022 outage affected multiple customers for about 1.5 hours.

Financial impact: Potential SLA payouts and lost future business.

Regulatory Risks:

Data privacy laws (GDPR, CCPA) require ongoing compliance efforts.

Content moderation issues could lead to legal challenges.

Potential for increased regulation of cloud and cybersecurity industries.

Cybersecurity Threats:

As a security provider, any breach could significantly impact trust.

Cloudflare itself is a high-value target for cybercriminals.

Reputational damage from a breach could be severe and long-lasting.

Technological Changes:

Rapid evolution of internet technologies requires constant innovation.

Risk of disruptive new technologies rendering current solutions obsolete.

High R&D spend (25.5% of revenue) necessary to stay competitive.

Geopolitical Risks:

International expansion exposes Cloudflare to various geopolitical risks.

Potential for service restrictions in certain countries.

Example: Cloudflare's decision to pull out of Russia in 2022.

9. Conclusion

Cloudflare presents a compelling investment case based on several key factors:

Strong growth drivers:

Consistent new customer acquisition

Successful upselling and cross-selling to existing customers

Direct benefit from increased usage of digital services

Emerging opportunities in AI and edge computing

Substantial growth runway:

Large and expanding TAM ($176 billion in 2024)

Current market penetration of only ~1.6% of estimated SAM

Potential for continued international expansion

Resilient business model:

High percentage of recurring revenue

Strong customer retention (112% dollar-based net retention rate)

Essential nature of services in an increasingly digital world

Competitive advantages:

Integrated platform offering security, performance, and reliability

Global network with presence in 330+ cities

Strong focus on innovation and product development

Developer-friendly approach fostering a growing ecosystem

Financial strength:

Consistent revenue growth (30% YoY in Q2 2024)

Improving profitability and cash flow generation

Strong balance sheet with $1.8 billion in cash and investments

Visionary leadership:

CEO Matthew Prince's track record of strategic decision-making

Ability to attract top talent and drive innovation

However, investors should also consider the risks, including intense competition, potential technological disruptions, and the current premium valuation.

In conclusion, Cloudflare's position at the intersection of critical internet infrastructure, security, and emerging technologies like AI and edge computing provides it with significant long-term growth potential. The company's execution in capitalizing on these opportunities while managing risks will be crucial in determining its future success and justifying its premium valuation.